简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

I'm a senior banker at Deutsche Bank. Here's why I'm worried about its bond business. - Business Insider

Abstract:Is Deutsche Bank's poor FIC performance transitory? Or is the division teetering as other European banks start to eat its lunch?

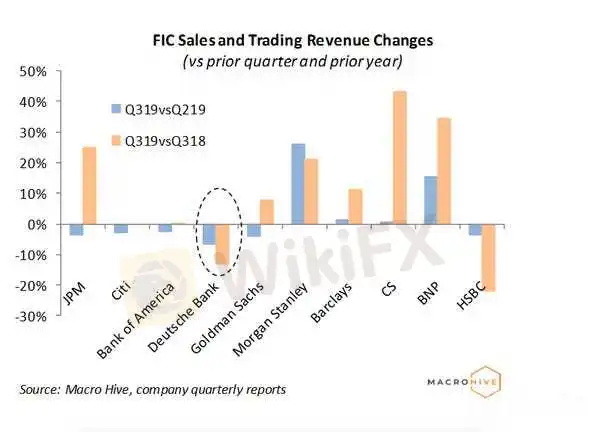

I'm a senior banker at Deutsche Bank. Robert James is my pen name. Over the next year or so, as the restructuring progresses, Deutsche Bank is likely to resemble a building site.Looking into poor FIC sales and trading revenues (a business to date left untouched by the restructure), we wonder whether there are early signs of structural erosion taking place.While feedback to the CEO of the restructure may have been positive, the real feedback is in clients trading with the bank. And that feedback has not been positive.This article originally appeared on Macro Hive. Read it here. Deutsche Bank stock fell over 10% on the release of its third quarter earnings last week. It has largely recovered since then, but is still underperforming the European bank aggregate this year. And over the past three years, Deutche Bank's stock has also lost over a third of its value. But what does the future hold?The latest earnings report augurs poorly for the long-term performance of the bank. It revealed a sizeable fall in Fixed Income and Currencies (FIC) revenues in the investment bank and continues to see DB management emphasise long-term plans rather than deal with immediate realities. The latest iteration of this emphasis is plans for radical transformation by 2022.So, a net loss of almost 1 billion euros was posted for the quarter – worse than analyst expectations of 772 million euros – but this was viewed as an afterthought against the apparent long-run earnings power of the bank.The press release around the earnings report was unironically titled “transformation on track.” But the reality is that over the next year or so, as the restructuring progresses, DB is likely to resemble a building site. Various one-off charges will limit any visibility of the type of investment bank that will eventually emerge.Management did emphasise recent strong loan growth compared to peers, centred on ABS and CRE, in the investment bank (17% y/y excl. FX, 22% incl. FX – perhaps reflecting a strong US weighting). But the question is, is DB overreaching at the wrong point in the cycle? No, according to CEO Christian Sewing; this growth simply reflected the bank now playing to its strengths with risk appetite unchanged.A teetering FIC franchise – are other banks eating DB's lunch?Looking into poor FIC sales and trading revenues (a business to date left untouched by the restructure), we wonder whether there are early signs of structural erosion taking place. Across the big banks this reporting season, a key trend was relative outperformance in FIC sales and trading: while revenues were generally down QoQ (quieter summer months, etc.), most banks performed well versus the prior year (Deutsche and HSBC being the exceptions).Between the US and Europe there was a slight twist on this theme, however. All the main US banks (except Morgan Stanley) reported lower QoQ FIC revenues, but in Europe most banks gained on the quarter – except DB, which saw significant erosion (down 7%). This theme also holds when comparing Q319 revenues versus Q318, begging the question: is DB's poor FIC performance transitory? Or is the division teetering as other European banks start to eat its lunch?

Macro Hive

Management thinks everything is fine. Clients' wallets are saying otherwiseDB's CFO James von Moltke naturally guided investors on his earnings call towards transitory factors. He cited problems in EM debt, restructuring in rates, a 37 million euro loss on a specific investment, and leadership changes early in the quarter. Meanwhile, DB's CEO Christian Sewing suggested that institutional clients had provided positive verbal feedback to the restructure.But it is natural to wonder whether the recent restructuring/turnover of staff has impacted the franchise on a longer term basis. This could be via lower client footprint or key staff leaving, which reduces the banks trading edge. So, while feedback to the CEO of the restructure may have been positive, the real feedback is in clients trading with the bank. And that feedback has not been positive. One to watch in the quarters ahead …And the Hard Place of Negative RatesAs for the management's emphasis on the long-term earnings potential of the bank, notably DB's 2022 revenue 'aspirations' of 25 billion euros, the last quarter's revenues annualise at only 21 billion euros. The higher aspiration number was created at the time of DB's July restructure. Now, the bank is admitting that interest rate headwinds have since emerged due to ECB monetary action in September.And while CFO von Moltke stated the bank is not sitting on its hands as this environment changes, he mentioned no specific measures beyond “looking for offsets.” On costs, CEO Sewing was more upbeat, citing reduced headcount. It is now below 90,000 for the first time since the Postbank acquisition. But headcount is actually growing on a like-for-like basis in the investment bank. He also highlighted lower costs, all currently in line with plans. But are cost cuts alone enough? The history of restructurings would suggest not.The bank's investor day on 10th December may provide more clues. But for now, the headwinds for DB are significant.Business Insider has reached out to Deutsche Bank for comment. Robert James (pen name) is a senior Deutsche Bank insider. Read the original article on Macro Hive here.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

AUS GLOBAL partners with the United Nations to promote Global Sustainable Development

We are honored to share that AUS GLOBAL, as an invited guest of the United Nations forum on Science, Technology and Innovation (UNSTI), successfully completed the important mission of this event on June 20, 2024 at the Palais des Nations in Geneva, Switzerland.The forum brought together dignitaries and renowned business people from around the world to discuss important topics such as global fintech development and environmental protection.

Tough truths about starting a business, from ban.do founder Jen Gotch - Business Insider

Jen Gotch, founder of accessories and stationery brand ban.do, said sometimes the best thing you can do is just say yes and figure it out later.

Morgan Stanley: 12 energy stocks to buy now as oil markets recover - Business Insider

After a historic oil price rout, energy markets appear set to recover. Morgan Stanley says these 12 oil and gas stocks will benefit most.

Bank of America hires Citi exec Diane Daley for AI governance role - Business Insider

Diane Daley spent over two decades at Citigroup, eventually serving as a managing director and the head of finance and risk management infrastructure.

WikiFX Broker

Latest News

Why Are Financial Firms Adopting Stablecoins to Enhance Services and Stability?

WikiFX

WikiFXExperienced Forex Traders Usually Do This Before Making a Lot of Money

WikiFXOcta vs XM:Face-Off: A Detailed Comparison

WikiFXWhen High Returns Go Wrong: How a Finance Manager Lost RM364,000

WikiFXBridging Trust, Exploring Best—WikiEXPO Hong Kong 2025 Wraps Up Spectacularly

WikiFXFidelity Investments Explores Stablecoin Innovation in Digital Assets Sector

WikiFXInteractive Brokers Expands Crypto Trading with Solana, XRP, Cardano, and Dogecoin

WikiFXSEC Ends Crypto.com Probe, No Action Taken by Regulator

WikiFXWhy More People Are Trading Online Today?

WikiFXBroker Comparison: FXTM vs XM

WikiFXCurrency Calculator