简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Stock market crash: Weak profit growth and recovery risk a new plunge - Business Insider

Abstract:Stocks need profit growth to rise on a sustained basis — but the coronavirus crisis is drying up cash flows.

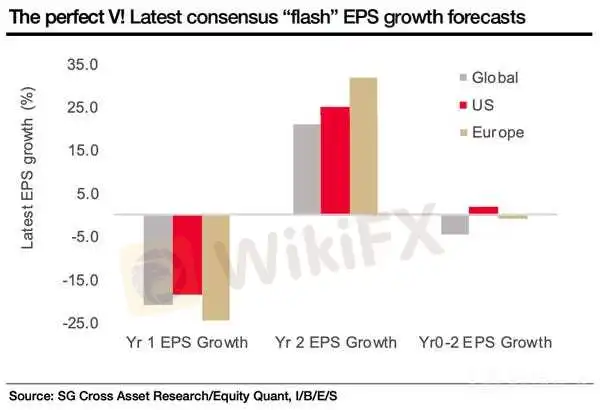

Andrew Lapthorne, the global head of quantitative research at Societe Generale, is skeptical of forecasts for a “perfect” v-shaped recovery in corporate earnings. The consensus forecast among analysts is that by the end of 2021, profits will be growing at nearly the same rate as they were in late-2019.Lapthorne considered the unique nature of this crisis and concluded that the consensus is too optimistic.Click here for more BI Prime stories.

Wall Street's expectations for recovery from the coronavirus crisis seems too good to be true. That's according to Andrew Lapthorne, the global head of quantitative research at Societe Generale. He is skeptical that the stock market's strong rebound from its trough in March matches up with the reality that will unfold in the months ahead. In particular, Lapthorne is skeptical of the “perfect” recovery that is reflected in real-time consensus forecasts for earnings, the biggest long-term driver of stock prices. Data he compiled shows that analysts expect global profits to fall by 21% this year and then rise 21% in 2021.In other words, the prediction is that economic conditions will recover so quickly that by December 2021, corporate profits will be back to where they were when COVID-19 began to spread in late-2019.

“Clearly this will not be the case,” Lapthorne said in a recent note to clients.

Societe Generale

In the alphabet soup of economic scenarios, analysts expect a V-shaped recovery that is turbocharged by effective containment of the outbreak and abundant government stimulus.Many countries around the world are clearly not close to fully reopening their economies. But the latter condition — stimulus — has been successful and unprecedented, ranging from the Federal Reserve's purchases of select junk-rated corporate debt to the checks wired straight to Americans' accounts.

Loading

Something is loading.

This helps explain why the S&P 500 has already retraced more than half of its losses after its fastest 30% decline ever. Once again, investors are buying equities knowing fully well that the Fed is ready to act as lifeguard.

“Yet there is zero evidence historically that markets can go up on a sustained basis whilst profits continue to slump,” Lapthorne said. “Equity markets may have bounced but investors still seem to be positioning themselves for a drop.”For proof of the ongoing risk to corporate profits, keep tabs on what companies are doing with their cash. Goldman Sachs strategists estimate that cash spending among S&P 500 companies will fall by a record 33% to $1.8 trillion this year. The decline includes cuts to dividends — another area where proof of cashflow constraints can be found. By adjusting for the expected drop in EPS this year, UBS estimates that the median S&P 500 dividend will fall 28% to $1.47. The largest expected dividend reductions are in cyclical sectors like energy and materials.Lapthorne is not the only strategist concerned that earnings expectations are still too high, even though they have been reined in by the pandemic.

“We are concerned 2021 numbers now need to be cut more aggressively,” said Lori Calvasina, the head of US equity strategy of RBC Capital Markets, in a recent note. Her 2021 EPS forecast that factors in a “healthy economic recovery and margin expansion” is $153, below the consensus forecast for $170.In addition, she noted that several executives have told analysts on earnings calls that the journey to get the economy back to its pre-coronavirus strength will be slow and uneven. These observations contrast the market's march higher — at least in Lapthorne's books. And the mismatch is one that may be corrected by another sell-off.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

Recession Concerns Ease: Can the U.S. Sustain Its Momentum?

The U.S. Conference Board Consumer Confidence Index rose to 100.3 in July 2024, up from a revised 97.8 in June. For Q2 2024, the U.S. GDP grew at an annualized rate of 2.8% in a preliminary reading, a notable increase from the 1.4% growth in Q1 2024. The Eurozone's annual Consumer Price Index (CPI) rose to 2.6% in July 2024, up from 2.5% in June. This slight increase was driven mainly by a jump in energy prices, which rose by 1.3% compared to 0.2% in the previous month. The US Core PCE which...

February 23, 2024- US Stocks Hit Record Highs, Tech Sector Fuels Rally

Nvidia Soars, European Markets Gain, and Key Forex Trends

Market Resurgence: Stocks Rally, Cryptos Surge, and Forex Fluctuations - February 15, 2024 Update

Key Insights into Today's Market Dynamics and Profitable Trading Strategies

EBC Research Institute Hotspot Analysis | China Unleashes Major Moves, Stock Market Brews a Violent Reversal

The Chinese government has taken measures to boost the stock market, yet the market still faces challenges, and investors should proceed with caution.

WikiFX Broker

Latest News

Germany's Election: Immigration, Economy & Political Tensions Take Centre Stage

WikiFX

WikiFXWikiFX Review: Is IVY Markets Reliable?

WikiFXBrazilian Man Charged in $290 Million Crypto Ponzi Scheme Affecting 126,000 Investors

WikiFXATFX Enhances Trading Platform with BlackArrow Integration

WikiFXBecome a Full-Time FX Trader in 6 Simple Steps

WikiFXIG 2025 Most Comprehensive Review

WikiFXConstruction Datuk Director Loses RM26.6 Mil to UVKXE Crypto Scam

WikiFXSEC Drops Coinbase Lawsuit, Signals Crypto Policy Shift

WikiFXShould You Choose Rock-West or Avoid it?

WikiFXScam Couple behind NECCORPO Arrested by Thai Authorities

WikiFXCurrency Calculator