简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Housing Is Hot With the Economy in the Deep Freeze

Abstract:A slowdown in construction and a halt to foreclosures squeezed supply, while low rates spurred demand.

No matter how you look at it, the economic fallout from the coronavirus is going to be brutal, with a projected 6.5% decline in real gross domestic product in 2020 and an unemployment rate of 9.3% at year-end, according to the Federal Reserve. In ordinary times, and without any policy response from government, a blow of this magnitude should weaken the housing market.

Yet, what we're starting to see is the very opposite. For various reasons, the supply of homes on the market continues to fall to record lows and home prices are, if anything, accelerating. For many homeowners stressed about the value of their biggest investment, it's a welcome relief. But this signals one more hurdle for would-be millennial homebuyers as they age into their family-forming years.

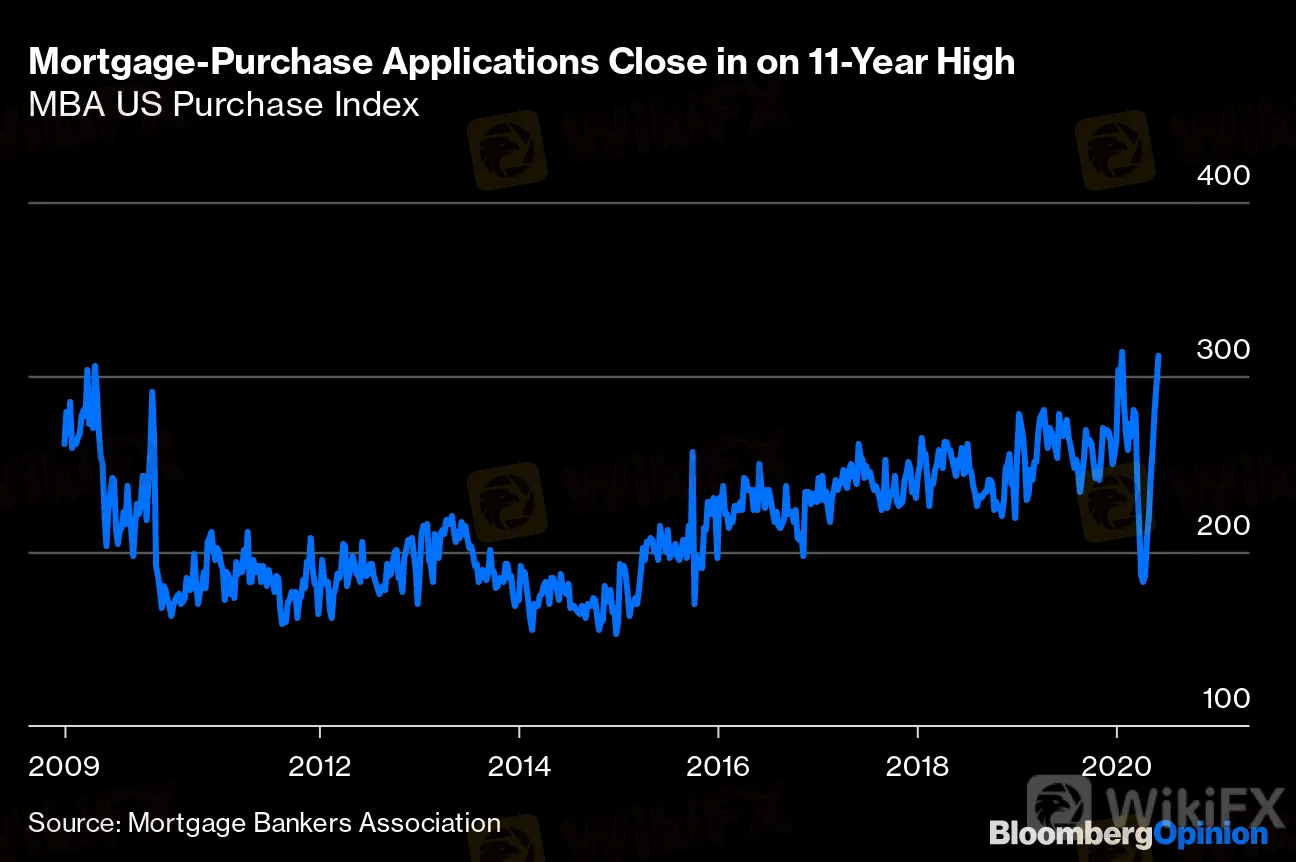

The biggest reason we're seeing home-price growth accelerating in the middle of a pandemic is that the disruption to the supply of housing is persisting longer than the disruption to demand -- that is, would-be buyers. Wednesday's weekly mortgage data showed that purchase applications rose for the eighth consecutive week and are approaching an 11-year high on a seasonally adjusted basis. Part of the reason for the quick rebound in demand is surely the decline in interest rates on mortgages to all-time lows, with few signs they are likely to rise for the foreseeable future.

Mortgage-Purchase Applications Close in on 11-Year High

MBA US Purchase Index

Source: Mortgage Bankers Association

But as is always the case in the housing market, supply doesn't respond as quickly as demand. Single-family housing starts plunged in March and April, with the most recent report showing a 25% year-over-year tumble. Part of this decline is because construction in some states shutdown, and much more so in some regions than others. Single-family starts fell 73% in the Northeast but only 13% in the South. Even where construction continued, the pace slowed as builders adopted social distancing and other health measures to prevent the spread of the coronavirus.

Even as demand rebounds, homebuilders may be slow to acquire new construction lots and might hold back on increasing production after getting the scare they did in March and April. They may prefer to wait a while to make sure these revived levels of demand are sustainable, while they also shore up their balance sheets before beginning to build at the same pace as earlier this year.

Beyond the impact on construction, a little discussed factor leading to fewer homes on the market is mortgage forbearance programs put in place by banks, states and Fannie Mae and Freddie Mac. From a policy standpoint it's great that banks and governments are helping to prevent a deluge of foreclosure as millions of people lose their livelihoods because of the pandemic. But a consequence of that policy change is that it deprives the housing market of the supply of foreclosed properties that occurs even in strong economies and solid job markets; this amounted to almost 500,000 houses in 2019.

Some homeowners may also be delaying the listing of their homes for sale because they're sheltering-in-place, or have lost their jobs and can no longer provide income verification to buy a different home. They may also not be comfortable having potential buyers, who could be carrying the virus, walking into their homes for sales showings.

Put it all together and housing supply continues to fall. Mike Simonsen of Altos Research, who tracks real-time housing data, notes that there are only 700,000 single-family homes for sale in U.S. compared to more than 900,000 at this time last year. Normally at this time of year the housing supply has been rising for a few months amid the traditional spring buying season, only to fall later in the year as activity slows. But that's not what we've seen during the past few months, as supply continues to contract. As a result, the percentage of homes for sale with price reductions is the lowest he's seen in his database, a leading indicator suggesting faster home-price growth in coming months.

Presumably, at some point the coronavirus crisis will pass, foreclosures will move forward again and all participants in the housing market from would-be buyers, sellers and homebuilders resume normal behavior. To the extent home prices rose too high because of supply distortions, we should see home prices leveling off or even declining. But it's not clear that this will be a 2020 story. And in the meantime, steadily rising home prices may join steadily rising stock-market prices in the middle of a pandemic as a phenomenon that continues to flummox everyone.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Brazilian Man Charged in $290 Million Crypto Ponzi Scheme Affecting 126,000 Investors

WikiFX

WikiFXBecome a Full-Time FX Trader in 6 Simple Steps

WikiFXATFX Enhances Trading Platform with BlackArrow Integration

WikiFXDecade-Long FX Scheme Unravels: Victims Lose Over RM48 Mil

WikiFXThe Top 5 Hidden Dangers of AI in Forex and Crypto Trading

WikiFXHow to Find the Perfect Broker for Your Trading Journey?

WikiFX5 Steps to Empower Investors' Trading

WikiFXThe Most Effective Technical Indicators for Forex Trading

WikiFXIG 2025 Most Comprehensive Review

WikiFXSEC Drops Coinbase Lawsuit, Signals Crypto Policy Shift

WikiFXCurrency Calculator