简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Trump Did Nothing to Help the Economic Boom

Abstract:If anything, the presidents actions were a minor drag on the recovery from the Great Recession.

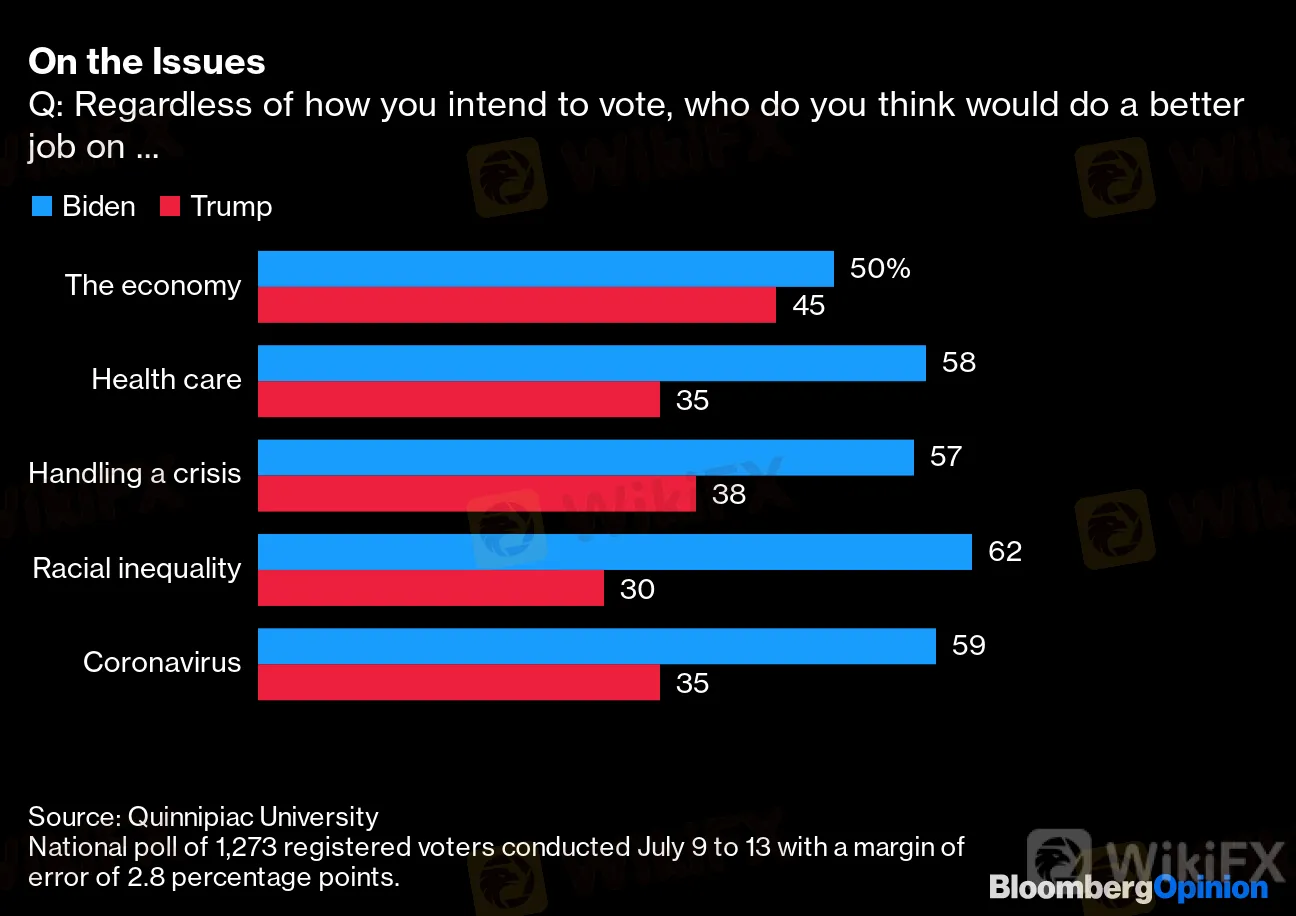

The public gives President Donald Trump very low marks for his handling of the coronavirus pandemic and race relations. But as recently as the end of June, the public was still giving him slightly positive marks for his handling of the economy. That edge may now be eroding, but Trumps numbers on economic policy are still much better than on other important issues:

On the Issues

Q: Regardless of how you intend to vote, who do you think would do a better job on ...

Source: Quinnipiac University

National poll of 1,273 registered voters conducted July 9 to 13 with a margin of error of 2.8 percentage points.

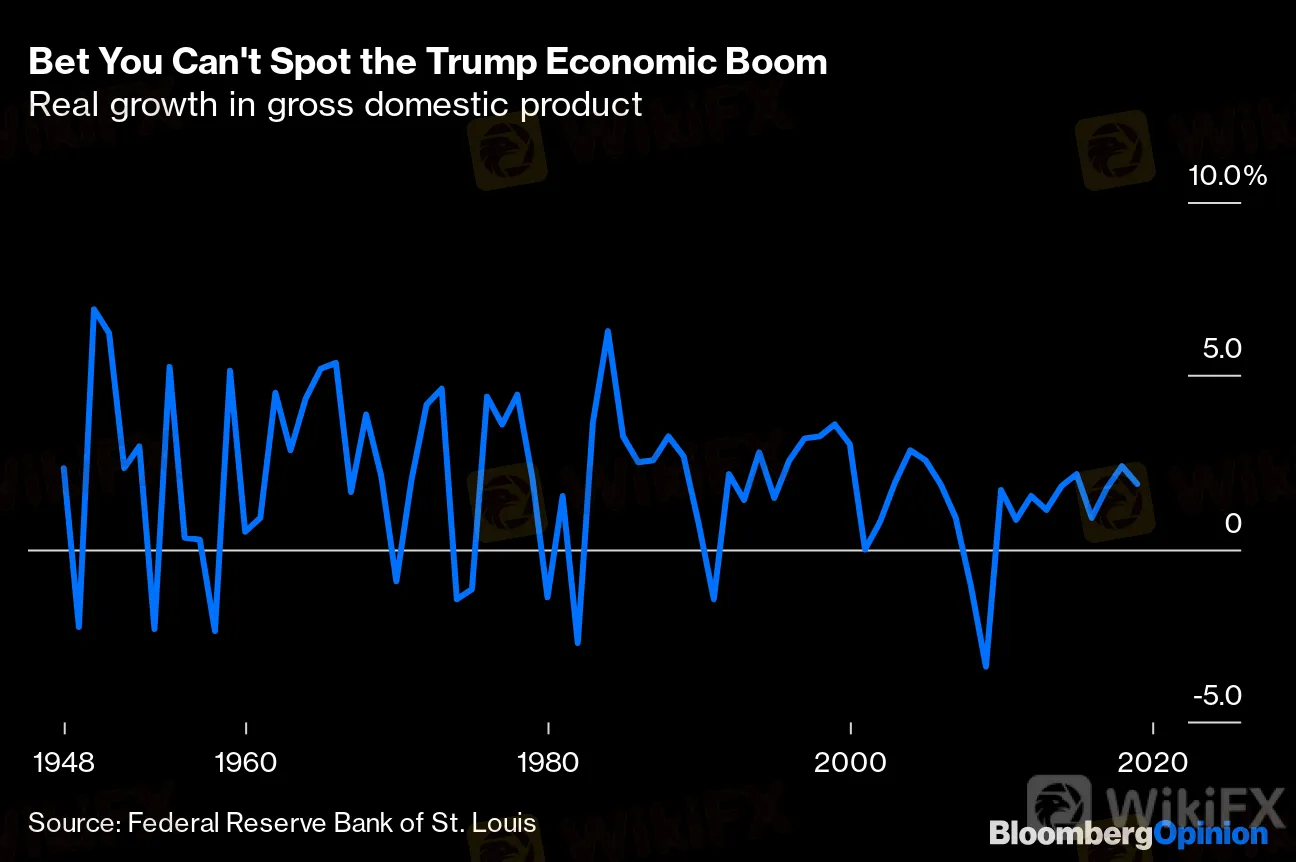

It‘s obvious why Trump gets decent ratings on the economy -- before the coronavirus outbreak in March, he had presided over the late stages of the longest economic expansion in postwar U.S. history. But the key phrase here is “presided over,” because Trump didn’t really do much more than that. If anything, those economic policies that he did manage to enact probably did more harm than good.

The expansion that began in 2009 was one for the history books, narrowly outlasting the booms of the 1990s and 1960s. But duration isnt everything. Much of the reason that recovery lasted so long is that there was such a big shock to recover from. In terms of growth in real gross domestic product per capita, that expansion was actually slower than most:

Bet You Can't Spot the Trump Economic Boom

Real growth in gross domestic product

Source: Federal Reserve Bank of St. Louis

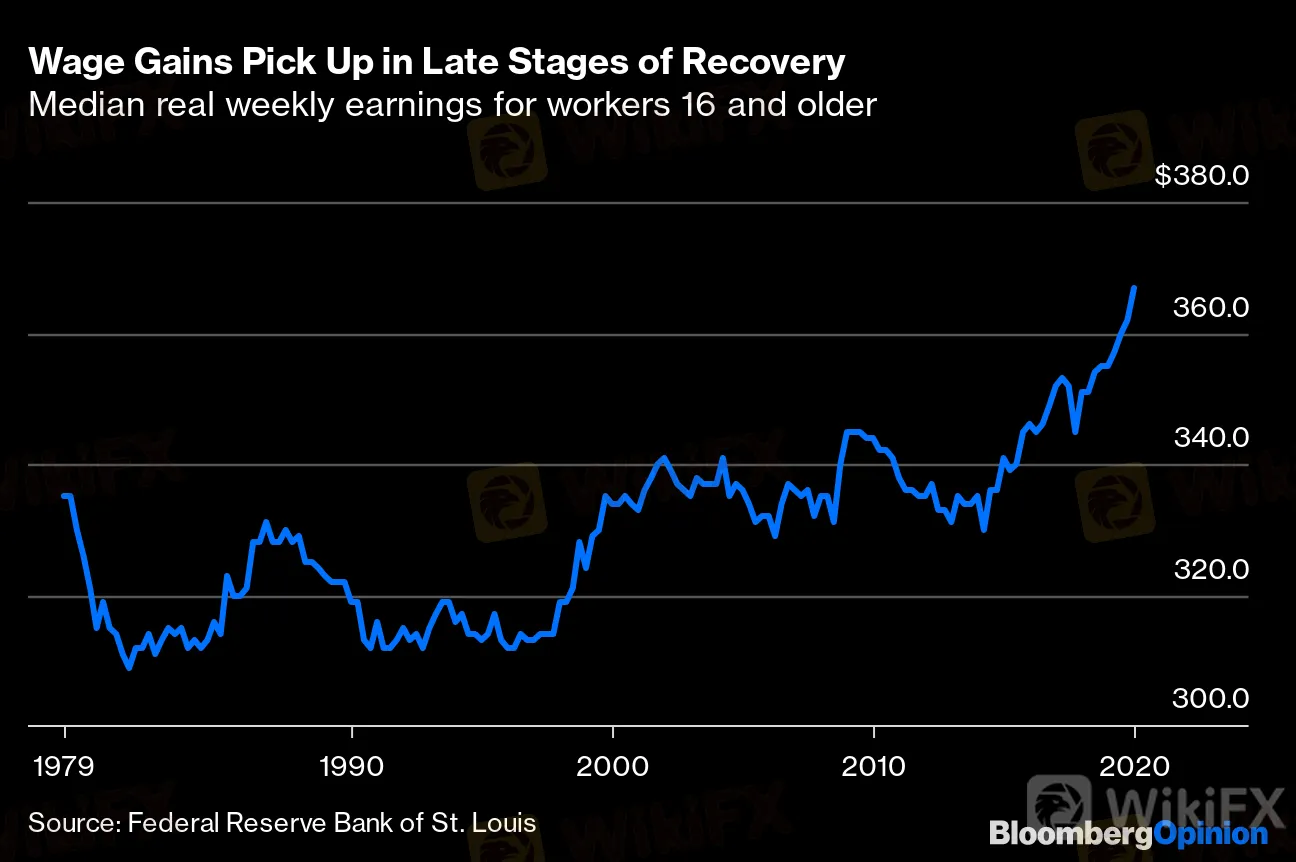

The one place where Trump‘s recovery shone was in terms of delivering economic gains to lower wage earners. Wages for the median full-time worker began rising strongly during President Barack Obama’s second term, and the rise continued under Trump

Wage Gains Pick Up in Late Stages of Recovery

Median real weekly earnings for workers 16 and older

Source: Federal Reserve Bank of St. Louis

More from

What‘s in a Name? NFL Team’s Decision Should Make Us Ask

Don't Hype the Hope for Oxford-AstraZeneca Covid Vaccine

Theyre All Friends in the Index

Chevron's $5 Billion Covid Bargain May Stand Alone

But this likely wasn't a function of anything Trump did; instead, it probably reflected the length of the expansion. Lower-wage workers with less education tend to be the first to get fired in a recession and the last to get hired when the economy recovers, meaning that their income gains tend to come only at the end of long periods of growth. Trump simply came into office at an opportune time.

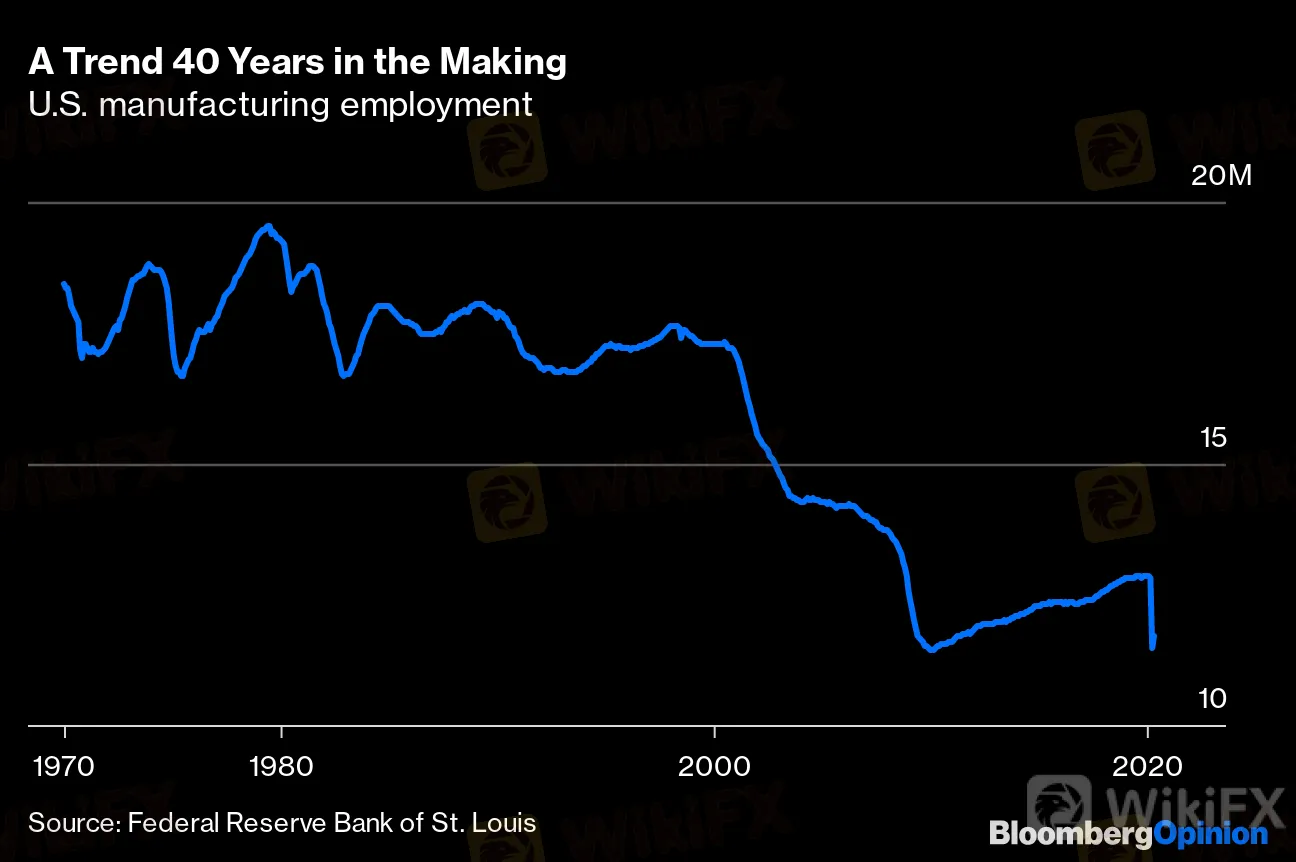

But to what extent should Trump get credit for keeping the expansion going? His diehard supporters will point to Trumps trade war, which was supposed to result in the reshoring of manufacturing jobs from China and elsewhere. The truth is that it did nothing of the sort. This recovery was unusually weak for factory jobs:

A Trend 40 Years in the Making

U.S. manufacturing employment

Source: Federal Reserve Bank of St. Louis

Trump‘s tariffs almost certainly made things harder for U.S. manufacturers by raising the price of imported components; steel tariffs, for example, increased costs for U.S. automakers. On top of that, the tariffs hurt consumption; multiple economic studies found that U.S. consumers were forced to pay almost all of the cost of Trump’s import taxes.

What about Trump‘s tax cuts? The impact of these is harder to gauge. Corporate tax cuts are supposed to fuel growth by stimulating business investment; if there’s no rise in investment, the policy probably isn‘t having much of an effect. A 2019 analysis by the International Monetary Fund and a 2019 study by the Congressional Research Service found that investment growth barely accelerated in response to Trump’s 2017 reforms. The longer-term impacts will be harder to gauge amid all the other factors affecting businesses‘ investment decisions since then. But the length of the economic expansion probably wasn’t because of the tax cuts.

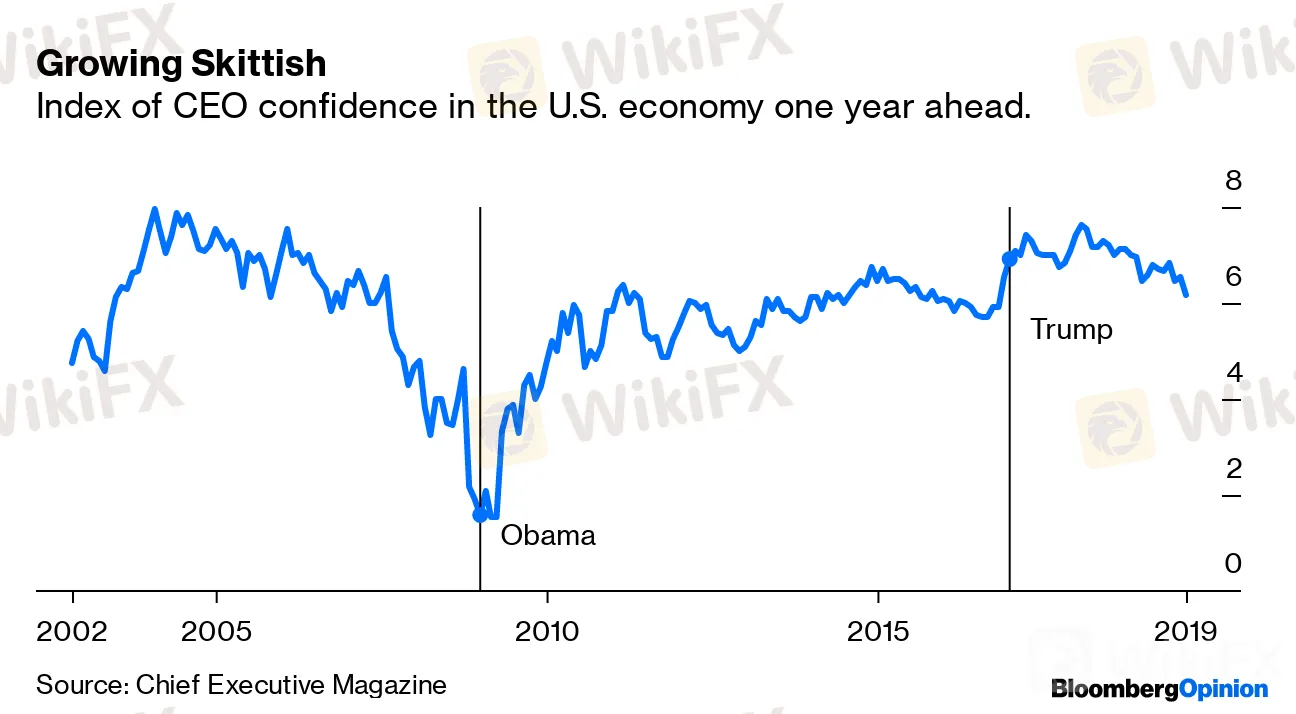

So if Trump‘s trade war hurt the economy slightly and his tax cuts had little immediate effect, how could Trump get credit for keeping the expansion going? The only possible way is through human psychology -- what economists call animal spirits. If business people -- who tend to lean Republican -- felt greater confidence from having a Republican in the White House, that might have made them more willing to invest. And indeed, measures of business confidence rose during the first two years of Trump’s presidency, though they began trending down in late 2018:

Growing Skittish

Index of CEO confidence in the U.S. economy one year ahead.

Source: Chief Executive Magazine

But even if Trump did give rise to a brief surge of economic optimism in 2017 and 2018, that‘s not a trick that can be repeated. Trump’s trade war was already sending business confidence lower, and now his disastrous coronavirus response promises to chill the economy for years to come.

Even this probably is giving Trump too much credit. The likeliest scenario is simply that he inherited a recovery from his predecessor, that this recovery lasted a long time because the economy was digging itself out of an unusually deep hole, and that Trump mildly hurt that recovery through bad trade policy. The private sector continued healing itself, assisted by low interest rates from the Federal Reserve. That many Americans still give him good marks on the economy is an unfortunate result of our tendency to give presidents too much credit for the actions of the others.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

TradingView Brings Live Market Charts to Telegram Users with New Mini App

WikiFX

WikiFXTrump tariffs: How will India navigate a world on the brink of a trade war?

WikiFXInteractive Brokers Launches Forecast Contracts in Canada for Market Predictions

WikiFXAuthorities Alert: MAS Impersonation Scam Hits Singapore

WikiFXStocks fall again as Trump tariff jitters continue

WikiFXINFINOX Partners with Acelerador Racing for Porsche Cup Brazil 2025

WikiFXRegulatory Failures Lead to $150,000 Fine for Thurston Springer

WikiFXApril Forex Trends: EUR/USD, GBP/USD, USD/JPY, AUD/USD, USD/CAD Insights

WikiFXMarch Oil Production Declines: How Is the Market Reacting?

WikiFXGeorgia Man Charged in Danbury Kidnapping and Crypto Extortion Plot

WikiFXCurrency Calculator