简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

The Fed May Not Recognize Inflation Until It's Too Late

Abstract:The central bank has a history of being behind the curve.

The Federal Reserve has come around to the conclusion that inflation isn‘t going to be a problem. So now it’s time to start wondering if inflation is going to be a problem. The Fed has a tendency to fight the last battle, which could lead policy makers to miss what may be the “Great Inflation” era.

The U.S. economy was unlikely to suffer an inflationary outbreak after the last recession simply because the Fed still retained too much fear of a 1970s repeat. In practice, its 2% inflation target made it appear that 2% inflation was a ceiling and overshooting that ceiling was never acceptable. The central bank based its policy on inflation forecasts rather than actual inflation even though those forecasts relied heavily on empirical estimates of the Phillips curve that posited a stronger relationship between unemployment and inflation than was revealed in the real world.

Recall that in September 2015, then Federal Reserve Chair Janet Yellen gave a long and detailed justification for the central bank to begin raising rates on the basis of the Phillips curve despite persistently low inflation. She proceeded to almost drive the economy into recession. Weak data and flailing financial markets forced the Fed to abandon its plans to tighten monetary policy after just one interest-rate increase in December 2015.

The history of the recovery from the Great Recession is that the Fed ensured inflation never really had a chance to get off the ground. In contrast, as I wrote last week, the Fed looks to learn from this experience, and may now attempt to overshoot the inflation target and downplay the Phillips curve by focusing on actual rather than forecasted inflation.

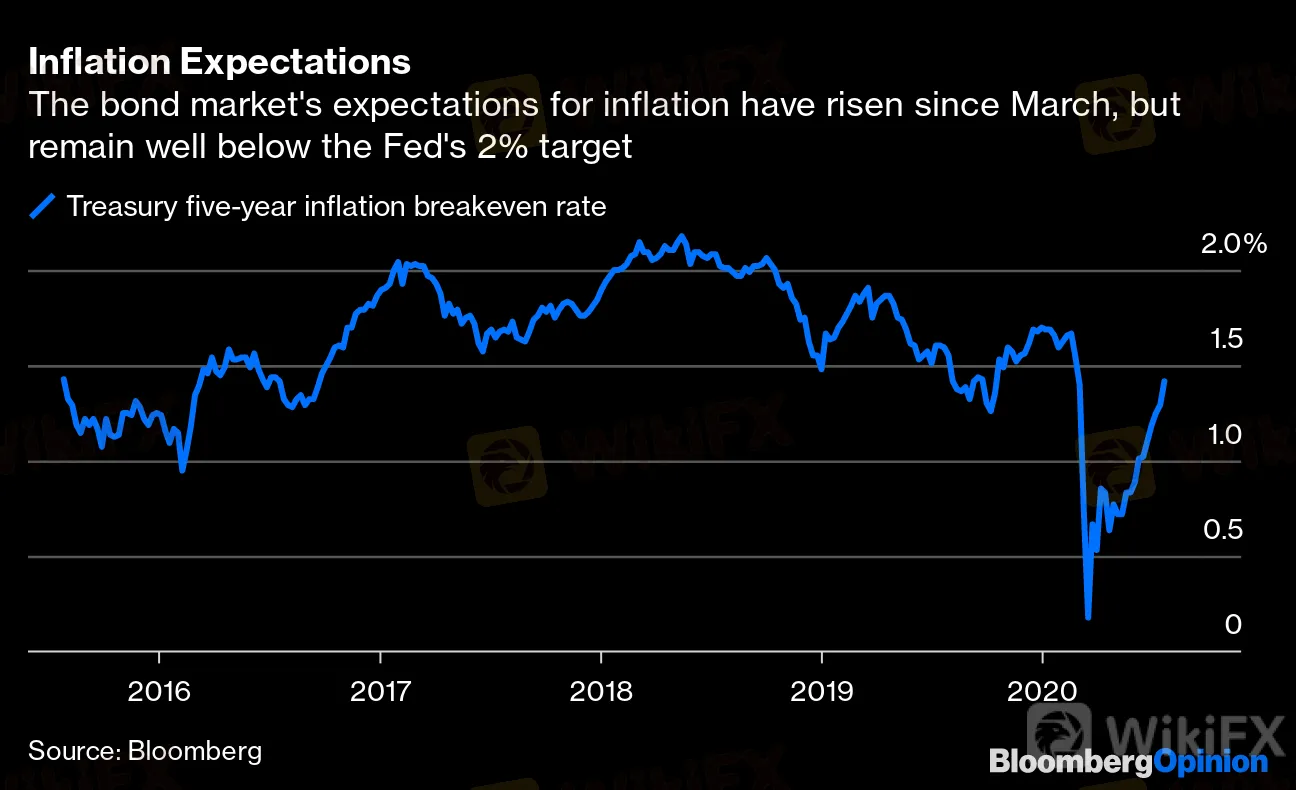

So now we have a new question to ask. Could the Fed go too far and kick off another period of high rates of inflation now that it no longer fears the 1970s? In the short term, the answer is “no,” or, are at a minimum, “very unlikely.” While a supply shock is an element of the current economic environment, the dominant issue right now is a massive negative demand shock that will weigh on near-term inflation. Although inflation expectations as measured by Treasury Inflation-Protected Securities have risen from their March lows, they are in no way suggesting an imminent inflation problem.

Inflation Expectations

The bond market's expectations for inflation have risen since March, but remain well below the Fed's 2% target

Source: Bloomberg

In the medium to long term the answer is “maybe.” I see three conditions as necessary to create a more interesting inflationary environment.

The first is that the economy faces persistent impediments to growing its productive capacity. Here the news doesn‘t look so good. The U.S. was already battling low productivity growth when the pandemic struck. It also faces lower fertility rates and likely lower rates of immigration. My Bloomberg Opinion colleague Conor Sen identifies shortages in housing, labor, health care, and child care that also limit the nation’s growth.

The second condition is ongoing, large-scale fiscal stimulus that props up demand while doing little to solve the above constraints to productive capacity. Dont interpret this to mean I am a deficit-scold. The current spate of fiscal stimulus to support incomes is very much needed to underpin demand and reduce further damage to the supply side of the economy. When the pandemic has passed, however, we should shift that spending toward policies that support growth. Otherwise, the risk will be higher that fiscal policy supports activity that outstrips our productive capacity.

The third condition is that the Fed ignores any warning signs that inflationary pressures are building. It is easy to see how this happens. The Fed typically fights the last battle. In the last recovery, this was still the battle against high inflation.

In this recovery, the battle will be against low inflation. Consequently, just as it downplayed weak inflation as “transitory,” the Fed will now be inclined to view high inflation the same way. In the last recovery, the Fed places much weight on estimates of the natural rate of unemployment. In this recovery, it is already rejecting those estimates in favor of trying to recreate the pre-pandemic labor market conditions.

Perhaps most importantly, it took years of evidence to convince the Fed that low inflation is a real problem. If and when the tide turns, it will take years before the Fed realizes high inflation is a problem. Inflation might not be a problem in the near term, but now that the Fed isnt concerned, it might finally be time to start thinking about how the inflation story might change.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Germany's Election: Immigration, Economy & Political Tensions Take Centre Stage

WikiFX

WikiFXWikiFX Review: Is IVY Markets Reliable?

WikiFXBrazilian Man Charged in $290 Million Crypto Ponzi Scheme Affecting 126,000 Investors

WikiFXATFX Enhances Trading Platform with BlackArrow Integration

WikiFXBecome a Full-Time FX Trader in 6 Simple Steps

WikiFXIG 2025 Most Comprehensive Review

WikiFXConstruction Datuk Director Loses RM26.6 Mil to UVKXE Crypto Scam

WikiFXSEC Drops Coinbase Lawsuit, Signals Crypto Policy Shift

WikiFXShould You Choose Rock-West or Avoid it?

WikiFXScam Couple behind NECCORPO Arrested by Thai Authorities

WikiFXCurrency Calculator