简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Bond Traders Crave Clarity. It's Not Here Yet.

Abstract:U.S. Treasuries quickly priced in a prolonged outcome that wont be easily unwound.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

Two things happened around 9:30 p.m. New York time on Tuesday as U.S. election results came pouring in:

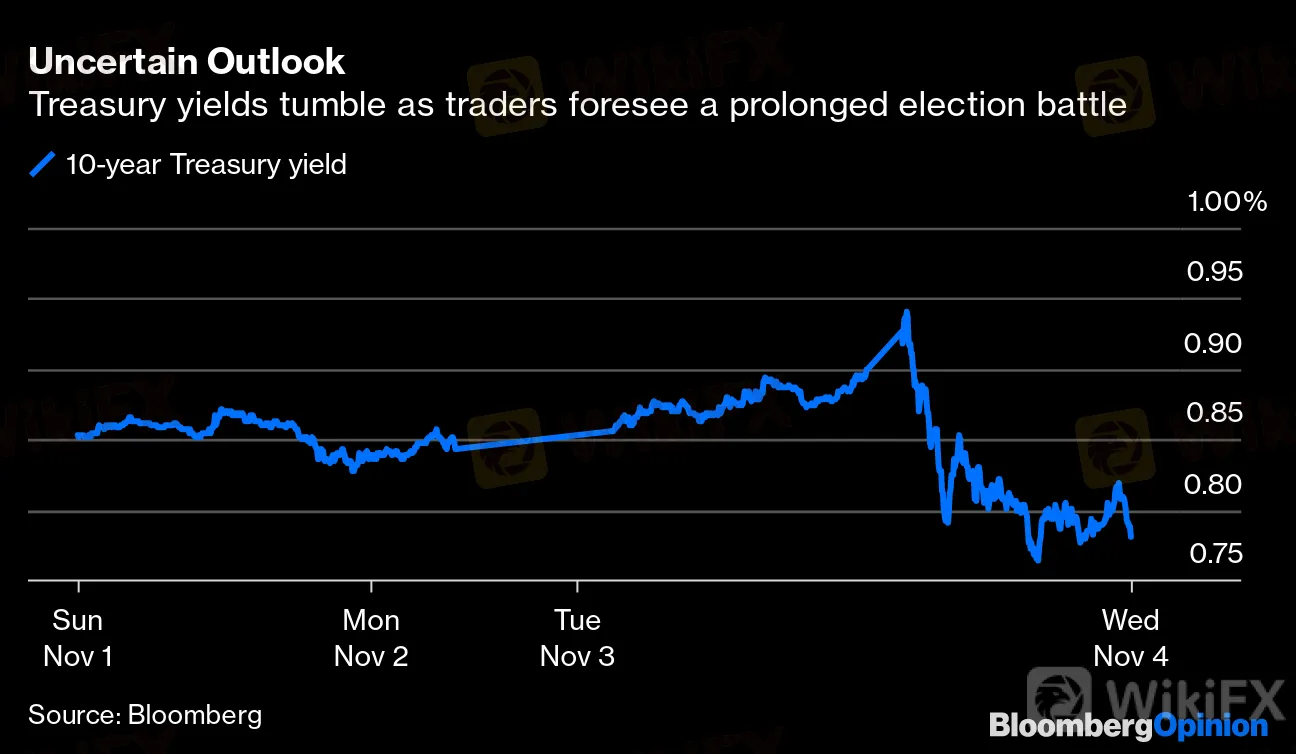

The 10-year Treasury yield extended its decline, touching 0.79% from as high as 0.94% about two hours earlier.

The odds of President Donald Trump winning re-election jumped to 71% from about 32% on Betfair.

Predictably, the second move received more attention, even though Betfair is a sliver of the size of the world‘s biggest bond market. After all, it seemed to reflect a dramatic shift that expressly captured bettors’ views on who would come out ahead in the presidential election. U.S. equities even began rallying in tandem with Trumps improving odds after previously soaring on the expectation that Democrat Joe Biden would emerge victorious and usher in a “blue wave.”

不确定观

债收益率翻滚,交易商预见延长的选举战斗

来源:Bloomberg

{7}

In hindsight, everyone would have been better off interpreting the clear signal from the huge rally in the $20.4 trillion Treasuries market: That this election has all the makings of a prolonged and contested affair. Long-term yields don‘t fall 10 basis points or more simply because one party is more likely to have control of the White House. Treasuries rally like that only when there’s an unexpected rush to havens — that is to say, when theres no clarity and investors are nervous.

{7}

{9}

Uncertain Outlook

{9}{10}

Treasury yields tumble as traders foresee a prolonged election battle

{10}

{12}

Source: Bloomberg

{12}

{15}

So it‘s little surprise that Treasury yields fell even further after Trump falsely claimed victory and said “we’ll be going to the U.S. Supreme Court. We want all voting to stop.” While this gambit was telegraphed well in advance, it‘s nonetheless unnerving for investors to see the world’s oldest democracy tested in such a way. It might take days before states such as Pennsylvania report final results, and even then, there could be challenges and recounts. Dont expect 10-year yields to test 1% under such a cloud of uncertainty.

{15}

More from

The Day Jack Ma Became Ray Dalio's Nightmare

Presidential Polling Fooled Us Twice. Cant Get Fooled Again

Polling Failed. It's Time to Kick the Addiction

Sorry, Boeing, the Yacht Had to Go

In reality, just about every state was more or less within the margin of error of polling expectations — it was simply that markets got a bit too eager to price in a “blue wave” scenario in recent days. The crucial battleground states of Wisconsin, Michigan and Pennsylvania appeared to favor the president early, but that mainly reflected Election Day votes, which tend to skew Republican. The unusually large number of absentee ballots cast because of the coronavirus pandemic, which lean Democratic, are still being counted there. Biden has already overtaken Trump in Wisconsin and Michigan.

This trend was known in advance, though it‘s fairly obvious that denizens of the election betting markets didn’t have a full understanding of this phenomenon. Jim Bianco, president and founder of Bianco Research, posted this map of PredictIt odds soon after 11 p.m. New York time, which showed Trump favored to sweep the Midwest battlegrounds:

{777}

As of this morning, Biden is not only competitive in two of those three states, but also in Georgia, where the New York Times‘s “needle” now gives the former vice president a razor-thin edge. When combined with leads in Nevada and Arizona and a pickup in Nebraska’s Second District, there are any number of ways for Biden to come out ahead.

{777}

Perhaps in a reflection of this shift, the 10-year Treasury yield climbed almost 5 basis points from its low, to 0.81% at 7:30 a.m. in New York, only to dive yet again to 0.76% by 9:20 a.m. Again, the craving for certainty above everything else is readily apparent here. A Biden presidency, combined with a Republican-controlled Senate and a weakened Democratic House majority, isnt exactly a recipe for the kind of fiscal stimulus that investors were imagining in their Democratic sweep scenarios. In fact, depending on whether you view Senate Majority Leader Mitch McConnell or House Speaker Nancy Pelosi as more obstructionist, this configuration is potentially the worst option for a fiscal jolt to the economy.

The only worse option in the eyes of bond traders, it seems, is a bitterly contested election. America might yet avoid that fate, but it certainly doesn‘t seem as if there will be a concession speech soon, either. As long as the country doesn’t know its next president, expect Treasuries to be a hot commodity.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Brian Chappatta at bchappatta1@bloomberg.net

To contact the editor responsible for this story:

Daniel Niemi at dniemi1@bloomberg.net

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Germany's Election: Immigration, Economy & Political Tensions Take Centre Stage

WikiFX

WikiFXWikiFX Review: Is IVY Markets Reliable?

WikiFXBrazilian Man Charged in $290 Million Crypto Ponzi Scheme Affecting 126,000 Investors

WikiFXBecome a Full-Time FX Trader in 6 Simple Steps

WikiFXATFX Enhances Trading Platform with BlackArrow Integration

WikiFXIG 2025 Most Comprehensive Review

WikiFXConstruction Datuk Director Loses RM26.6 Mil to UVKXE Crypto Scam

WikiFXSEC Drops Coinbase Lawsuit, Signals Crypto Policy Shift

WikiFXShould You Choose Rock-West or Avoid it?

WikiFXScam Couple behind NECCORPO Arrested by Thai Authorities

WikiFXCurrency Calculator