简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Next stock market crash: Investor returns face new, post-crisis threat - Business Insider

Abstract:The era of lower interest rates adds a new challenge to the fund management industry that is already battling asset outflows and lower fees.

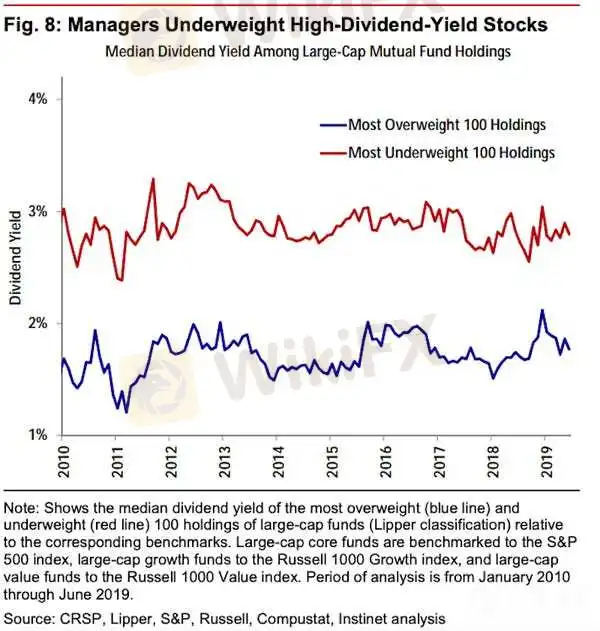

The era of persistently lower interest rates has introduced a new risk to the already challenged fund-manager industry.Joseph Mezrich, the head of equities quantitative strategies at Nomura, explained in a recent note why fund performance could be persistently lower, and what fund managers can do to remedy this.Click here for more BI Prime stories.One of the defining features of the era since the Great Recession for investors has been the prevalence of low interest rates. Equity fund managers have not been exempt from the impact of this trend. In fact, their portfolios have felt the pain over the past 40 years whenever interest rates fell, according to Joseph Mezrich, the head of equities quantitative strategies at Nomura. The reason, he said, is that interest rates tend to fall when the economy is not doing well and rise when conditions are on the upswing. Concurrently, the diversity of smaller, domestically oriented firms that stock pickers can profit from usually increases when rates are rising. The reverse is typically the case: lower rates and expectations for the economy limits the number of stocks that investors can pick from.But there are new ways in which low interest rates are hurting active funds' performance — and this pain could continue to if managers do not course-correct, Mezrich said in a recent note to clients. What is new post-crisis is that low interest rates have fueled the rise of stocks that offer the kinds of yields investors earned when rates were structurally higher. Since 2011, these so-called bond proxies that are part of the Russell 1000 have consistently offered dividend payouts that exceed the 10-year yield, Mezrich said. The problem is that despite this built-in advantage, active fund managers have tended to underweight high-dividend-yield stocks and overweight low-dividend-yield stocks, positioning their portfolios in a manner that does not benefit them, Mezrich said. He illustrated his point with the following chart:

Nomura

He sees this trend potentially crimping performance going forward, and compounding the challenges that the mutual-fund industry is already confronting.Every year since 2016, more mutual funds have closed shop than have opened, according to data compiled by Morningstar. That's the longest streak of net-negative change going back to at least 1999. Active fund managers will likely continue facing headwinds “if America goes the way of Japan, with interest rates drifting towards zero, and if current cost-cutting trends in the financial services industry continue,” Mezrich said.Remedies for the futureThe good news is that there are ways to address these challenges. Mezrich's first suggestion is that the fund industry stops blaming the wrong culprit for much its underperformance. The usual suspects include quants, who are able to quickly spot mispricings in the market and exploit the same opportunities that stock pickers want for themselves. Moving forward in a lower-interest-rate world, one way to remedy fund underperformance is to flip the script and gain more portfolio exposure to the high-dividend-yielding stocks they were previously underweight. Mezrich also proposes that fund managers become aware of how low portfolio turnover — the frequency with which stocks are bought and sold — can hurt their performance. He describes it as avoiding the “momentum trap.” When a fund's performance becomes driven by a few outperforming stocks, it inevitably becomes exposed to the downside scenario. We saw this firsthand in September when many of the market's favorite growth stocks fell out of bed. “Increasing portfolio turnover may be the simplest corrective for this 'momentum trap,'” Mezrich said. “More generally, control of unintended momentum tilts by optimization or momentum factor hedging would help.”

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

EBC Research Institute Hotspot Analysis | China Unleashes Major Moves, Stock Market Brews a Violent Reversal

The Chinese government has taken measures to boost the stock market, yet the market still faces challenges, and investors should proceed with caution.

How does the Stock Market Volatility Impact Forex Trading?

While the Stock market and the Forex market are two of the most significant components of the global financial system, interestingly, both are closely interconnected. It is no secret that stock market volatility can affect various aspects of the economy, but how does it affect Forex trading? Join us on this journey to learn how volatility in the stock market affects Forex trading and what forex traders can do to mitigate risks and seize opportunities!

How does the Stock Market Volatility Impact Forex Trading?

While the Stock market and the Forex market are two of the most significant components of the global financial system, interestingly, both are closely interconnected. It is no secret that stock market volatility can affect various aspects of the economy, but how does it affect Forex trading? Join us on this journey to learn how volatility in the stock market affects Forex trading and what forex traders can do to mitigate risks and seize opportunities!

Asian Stock Market Updates

Asian stocks extend global rally to 7th day, U.S. stimulus in focus.

WikiFX Broker

Latest News

Exposing the Top 5 Scam Brokers of March 2025: A Closer Look by WikiFX

WikiFX

WikiFXGold Prices Climb Again – Have Investors Seized the Opportunity?

WikiFXWebull Launches SMSF Investment Platform with Zero Fees

WikiFXAustralian Regulator Warns of Money Laundering and Fraud Risks in Crypto ATMs

WikiFXThe Withdrawal Trap: How Scam Brokers Lure Victims into Paying More

WikiFXFCA to Investors: Think Twice Before Trusting These Brokers

WikiFXTrump\s tariffs: How could they affect the UK and your money

WikiFXTrump gambles it all on global tariffs he\s wanted for decades

WikiFXHTFX Spreads Joy During Eid Charity Event in Jakarta

WikiFXHow Will the Market React at a Crucial Turning Point?

WikiFXCurrency Calculator