简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

European Rescue Fund Creates a New Big Beast in Bond Market

Abstract:Paying for the EUs recovery fund through bond sales should be a breeze.

Congratulations to the European Union for agreeing a groundbreaking deal to distribute 750 billion euros ($864 billion) of grants and loans among its 27 members to bolster the recovery from the pandemic. Now it has to find a way to pay for it. And bond investors are ready, willing, able and eager to help.

Step forward an oven-ready vehicle already used by the European Commission, which already borrows in the name of the EU to satisfy centralized funding needs in the bloc. The Commission can tap the highly liquid bond market to pay for the rescue fund, with the financing spread out over the next seven years in line with the EU budget framework. The actual debt maturities will be much longer and will be spread out across the yield curve, allowing for a lot of flexibility to adjust bond sales to wherever investor demand is strongest.

Austria‘s recent successful issue of its second 100-year bond illustrates there’s investor appetite for high-quality assets offering any hint of a yield — or even something whose rates aren‘t as negative as other European benchmarks. It also suggests that there’s no upper limit on how long-dated EU bond issues can be, although as markets enter the summer quiet period, it will be wise to tread carefully in assessing investor interest. It will likely initially issue in more liquid maturities such as 5- or 10-year terms before selling longer-dated bonds.

Before long, EU debt will be totally interchangeable with the other liquid sovereign debt issued by European countries. It will become part of the capital markets furniture.

With the European Central Bank‘s bond-buying program hoovering up so much of the German bund market, investors are sorely in need of a so-called safe asset. EU debt fits the bill, with credit ratings of AAA from Moody's Investors Service and AA from S&P Global Ratings. The existing market for EU-issued debt issued is small, at just 51 billion euros, of which almost 10 billion euros matures next year, so a boost in supply will meet a need. Annual issuance is in line to increase by 150 billion euros or more, roughly equivalent to a large European country’s needs.

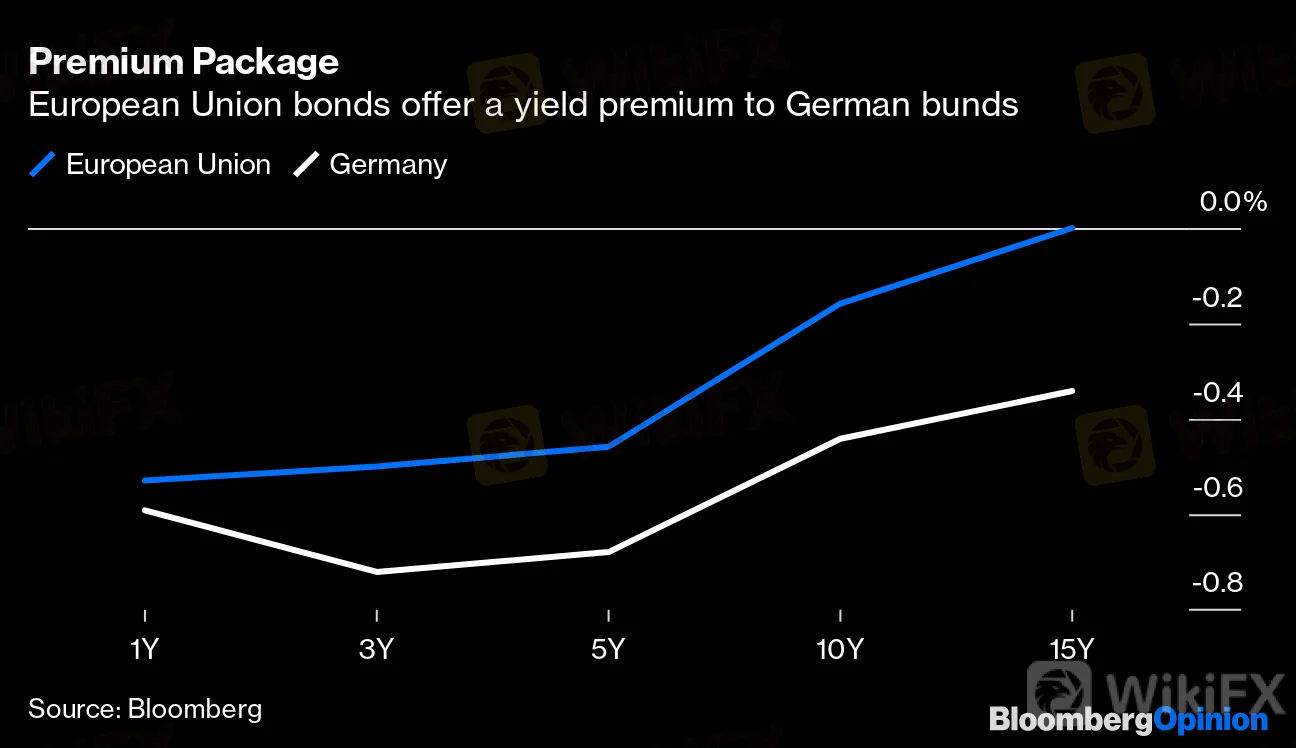

Moreover, with the euro zones benchmark debt yields in deeply negative territory — investors pay about 44 basis points for the privilege of lending to Germany for a decade — the premium offered by EU bonds gives bondholders some relief, albeit still at yields below zero. And the new pandemic bond issues might well offer positive yields given their vastly bigger size and the need to keep them attractive.

Premium Package

European Union bonds offer a yield premium to German bunds

Source: Bloomberg

And the prospect of a massive increase in the supply of EU bonds hasnt frightened the horses. The most recent issue in its name, 500 million euros of 15-year bonds sold at the beginning of last month, has steadily improved in value, driving the yield down to just below zero from an initial level of about 0.2%.

Mr Spielberg Will See You Now

The EU bond vehicle shows it is ready for its big moment as yields have steadily fallen since the most recent issue was sold in early June

Source: Bloomberg

EU debt is already the closest thing to a common bond that exists in the bloc. Needs must: Germany has overcome its mistrust of debt mutualization in its desire to keep the union intact and sanctioned a flood of securities that are euro bonds in all but name. The rescue package may not meet the definition of a Hamilton moment, but it marks a true turning point in the EUs relationship with the capital markets.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Germany's Election: Immigration, Economy & Political Tensions Take Centre Stage

WikiFX

WikiFXWikiFX Review: Is IVY Markets Reliable?

WikiFXBrazilian Man Charged in $290 Million Crypto Ponzi Scheme Affecting 126,000 Investors

WikiFXATFX Enhances Trading Platform with BlackArrow Integration

WikiFXBecome a Full-Time FX Trader in 6 Simple Steps

WikiFXIG 2025 Most Comprehensive Review

WikiFXSEC Drops Coinbase Lawsuit, Signals Crypto Policy Shift

WikiFXConstruction Datuk Director Loses RM26.6 Mil to UVKXE Crypto Scam

WikiFXShould You Choose Rock-West or Avoid it?

WikiFXFranklin Templeton Submitted S-1 Filing for Spot Solana ETF to the SEC on February 21

WikiFXCurrency Calculator