简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Government Shutdown Weighs on GDP, Business-Leader Confidence

Abstract:As the government shutdown drags on, investors are becoming increasingly concerned with the likelihood of a recession as business leader confidence dips.

Government Shutdown Talking Points:

As the government shutdown enters its 30th day, it continues to sap 0.13% from GDP per week according to the White House

United States GDP was already forecasted to slip moderately but that information has been masked by the lack of economic data released

On the other hand, soft data like business leader sentiment has dropped sharply amid the shutdown

See Q119 forecasts for the Dow, Dollar, Bitcoin and more with the DailyFX Trading Guides.

Economic data from the world‘s largest economy has been halted for the last month as the government shutdown continues to chip away at US GDP each week. Prior to the shutdown, US GDP was already slated to decline steadily as the impact of President Trump’s tax cuts fade. To compound this, a week of government closure equates to a -0.13% hit on total GDP according to the White House. Now that economic data is sparse, investors and economists are effectively flying blind.

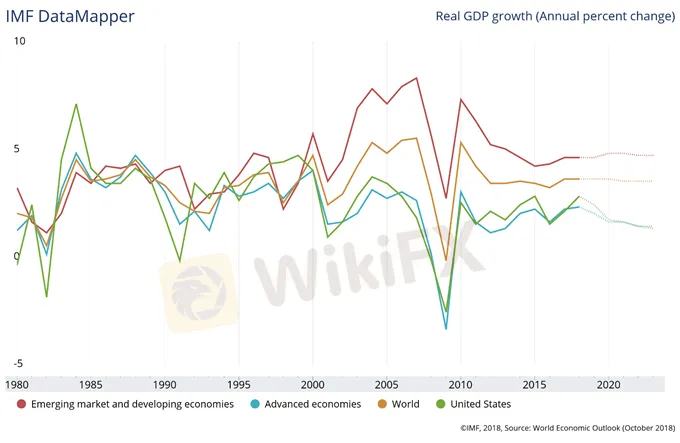

Global GDP Forecasts (Chart 1)

In lieu of hard data, investors look to sentiment and confidence readings to bridge the gaps. In a recent PwC survey, nearly 30% of 1,300 business leaders believe global growth will decline in the next twelve months. The level of pessimism is roughly six-times higher than it was one year ago.

Notably, the largest shift in sentiment came from North American executives. Optimism dropped from 63% to 37% in 2018 to 2019 and aligns with survey results from Boston Consulting Group conducted late last year which found 73% of respondents see a recession within the next two years.

S&P 500 Price Chart Daily Timeframe, October 2018 – January 2019 (Chart 2)

While the S&P 500 seems to be taking the lack of information in stride, negative impacts will only be exacerbated as the shutdown continues. With each day the government is shuttered, the pace of contraction will only grow steeper. Further, once the government is re-opened and data like the Federal Reserve Bank of Atlantas GDPNow model begin to cross the wires once again, the data gap could deliver a shock to newly reported figures.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

High Volatility Economic Events for This Week (GMT+8)

This week, key economic events expected to generate high volatility include China's Q2 GDP and retail sales data, impacting CNY. The US will release Core Retail Sales and Philadelphia Fed Manufacturing Index, affecting USD. The UK's CPI data will influence GBP, and the ECB Interest Rate Decision and Press Conference will impact EUR. These events will drive significant market movements due to their influence on monetary policy and economic outlooks.

US Dollar Price Outlook: EUR/USD Eyes GDP, Trade Balance Data

The US Dollar could be at risk in light of upcoming economic data releases during Thursday's trading session with Q2 GDP and July Advanced Goods Trade Balance serving as potential catalysts for volatility.

GBP/USD: Pound Sterling Eyes Q2 GDP Amid Rising Brexit Risks

The British Pound faces major event risk with UK Q2 GDP data due for release Friday which looks to provide the latest health check on the British economy amid prolonged Brexit uncertainty.

Feds Powell Shakes the Dow and Dollar as Markets Confused on Next Steps

The Fed cut rates for the first time in over a decade by 25bp to 2.00-2.25% seeming to keep options for more on the table

WikiFX Broker

Latest News

Will Gold Prices Continue to Rise Due to Trump’s Tariffs?

WikiFX

WikiFXMiami Firm Owner Pleads Guilty to $6M Ponzi Scheme Fraud

WikiFXeToro Files for IPO with $5 Billion Valuation on NASDAQ

WikiFXNBI Cebu Arrests Forex Trader for Illegal Investment Solicitation

WikiFXPU Prime's "Feather Your Trades" Contest! Begin

WikiFXIs FizmoFX a Scam? Fraud and Account Suspension of Traders

WikiFXIG Japan Extends US Stock CFD Trading Hours in 2025

WikiFXWhich Zodiac Sign Makes the Best Trader?

WikiFXALERT! Warning against Livaxxen

WikiFXVanguard Settles $106M SEC Case Over Misleading Investors

WikiFXCurrency Calculator